This is Part II in the Gridtech's Moneyball 3-part series:

- Part I: What utilities buy

- Part II: 5 Utility buying signals

- Part III: Signal into strategy

---

In baseball, scouts once trusted their gut before spreadsheets. Gridtech is having it’s own Moneyball moment, and instinct is being built together with evidence.

For years, selling into utilities has been like trying to win over a glacier with a sales deck. Long RFPs, slow budgets, and polite “circle backs” that last whole fiscal quarters. Founders have been burning the runway while waiting for the next committee meeting. Each update is a flare shot into the sky (and half the industry misses it while refreshing their CRM).

Now, AI and a new wave of digital scouts have turned those hidden movements into visible signals.

“Utilities shift when pressure builds from mandates, funding windows, grid constraints, or new hires.”

Each of those moments leaves traces, which we call buying signals. You can think of them as breadcrumbs; small, public indicators that a utility is preparing to commit. They are proof foundations are well underway and that construction towards the solution is about to begin.

Data scouts don’t guess, they just keep better box scores.

Let’s step into the scout’s dugout and see where the data is actually pointing.

1. Regulatory Filings

Signal strength: High early indicator 🟢

Before procurement comes paperwork, and before paperwork comes compliance strategy.

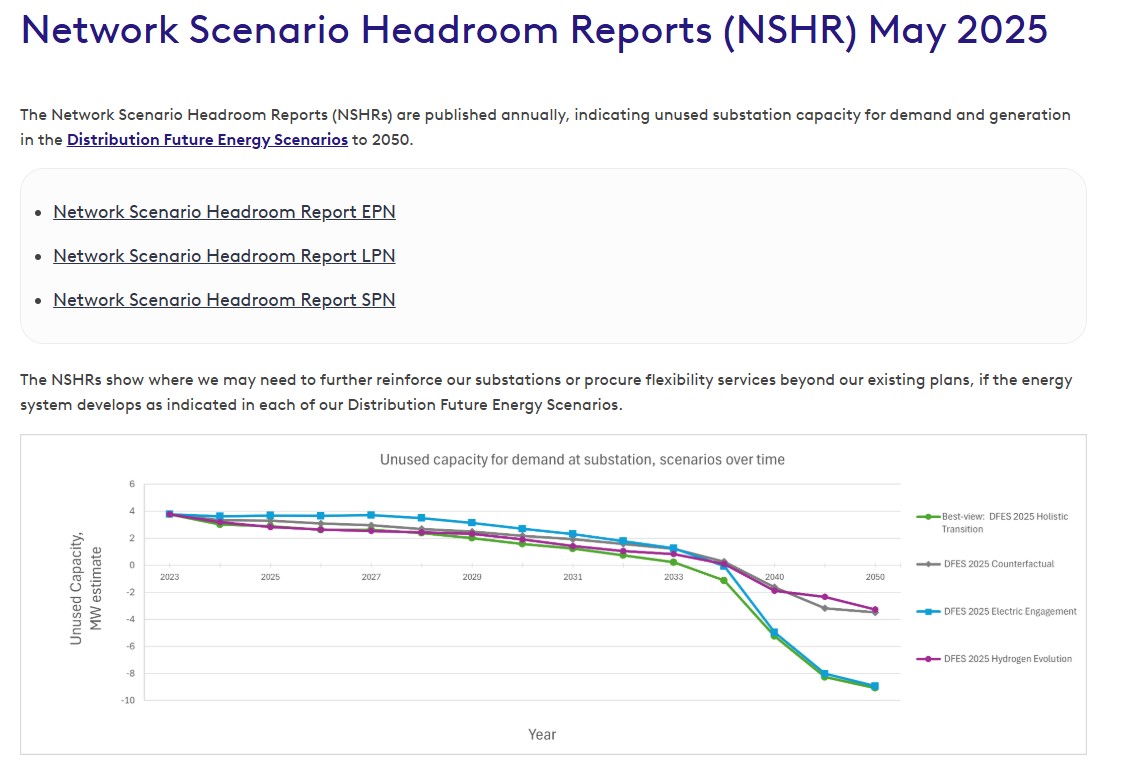

Regulation is the cleanest signal in the game, even if it operates on longer timeframes. Every time a docket mentions “grid reliability” or “customer flexibility,” we are seeing tomorrow’s budgets.

That’s because every new target or reporting rule creates internal deadlines, and deadlines become budgets. Economists call this regulatory signaling: the earliest public hint that money will move.

Let’s read the box score across regions.

European Union

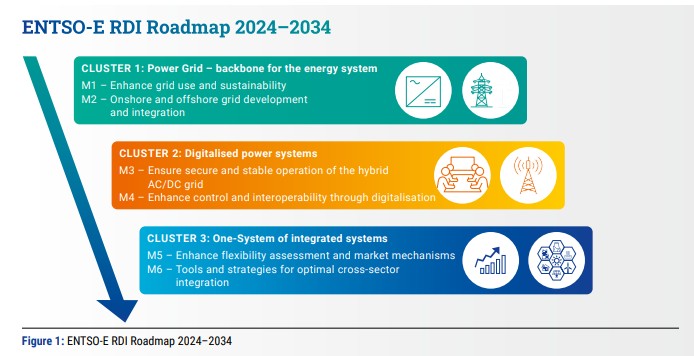

The Grid Action Plan (EC 2023) and ENTSO-E’s Distributed Flexibility Roadmap set measurable milestones for digitalisation and demand-side participation.

Each release triggers feasibility studies, resourcing, and signals hidden in at least three PowerPoints; all useful but nonetheless nobody will admit to not reading them.

Specific awards like the TEN-E funding corridors reveal where grid-digitalisation pilots will land next, which includes European Commission project funding for Energy, Climate change, and Environment.

United Kingdom

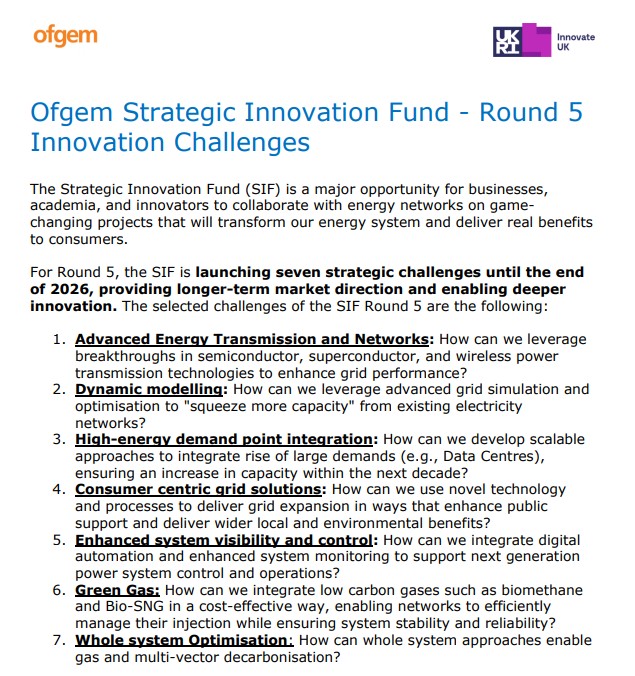

Ofgem’s Strategic Innovation Fund (SIF) and Digitalisation Strategy updates act as early indicators of where new pilots will form.

United States

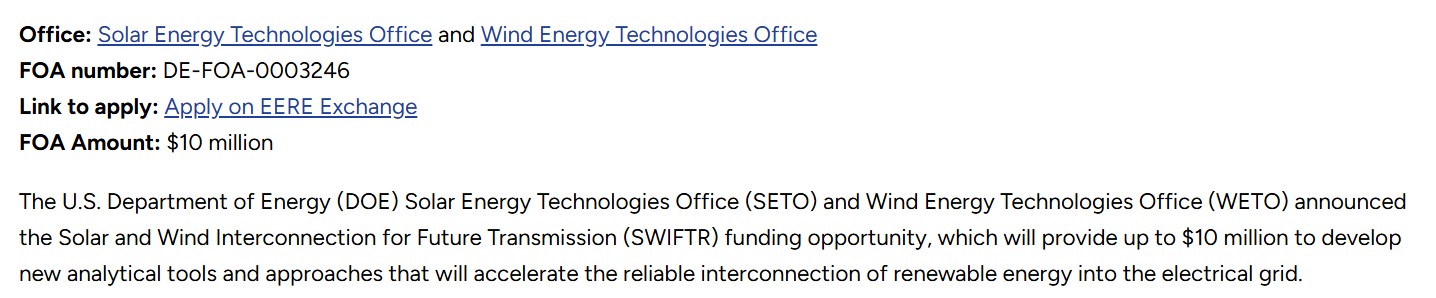

Federal funding may have cooled, but state-level Integrated Resource Plans (IRPs) and FERC Order 2222 compliance filings still mark where distributed-energy programs are growing. A utility publishing a 2025 IRP that includes non-wires alternatives is effectively announcing its next budget focus.

While regulatory volatility means we need to cautious of pulled projects, the i2x DOE interconnection roadmap lays out a well-thought out plan and includes five target metrics for 2030 that can be measured using publicly available data.

From this plan, funding projects follow in line.

For commercial teams, this means we can treat new policy targets like product launches. As long as we mark the dates and plan around them, we can be ready ahead of one or two budget cycles, when procurement follows.

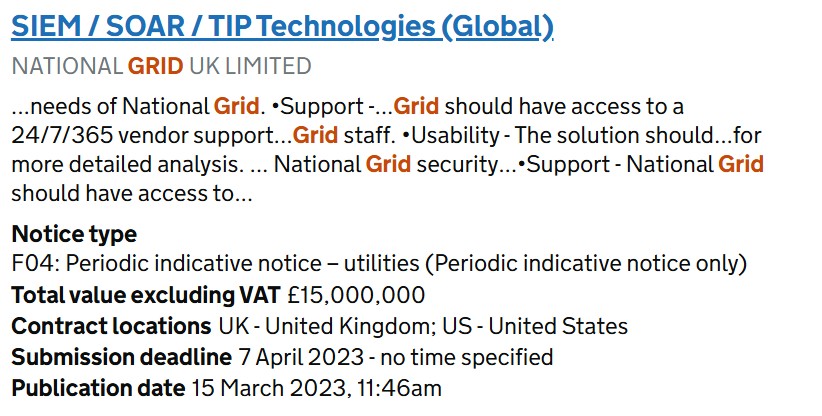

2. Procurement and RFP Signals

Signal strength: Medium to High, confirmation of budget activation 🟢

Public procurement is the scoreboard that follows internal strategic planning. By the time an RFP hits, the real game has already started playing out behind the scenes. That's why staying on top of regulatory filings is important; if you only start chasing RFPs when they drop, you’re already late to the ballpark.

Let’s see what these processes look like for different markets.

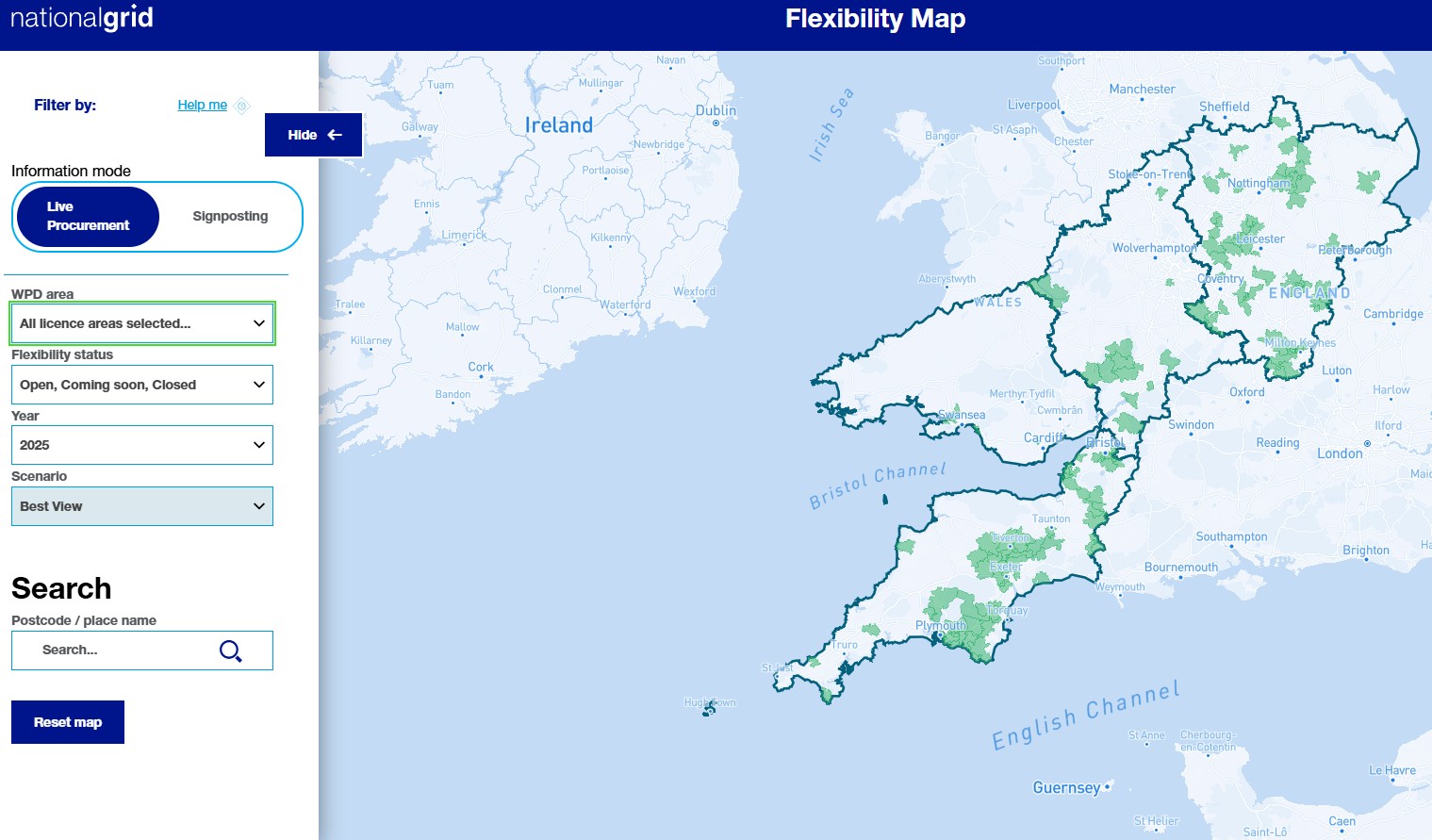

In the UK, competitive procurement for flexibility is now standard.

1. All six DSOs operate markets through their own platforms and through the Dynamic Purchasing System (DPS).

2. When a new DPS notice appears, it signals an open window for approved suppliers.

3. Framework refreshes typically happen annually and are followed by multiple local tenders within six to nine months.

4. You can use the Find a Tender service to search for keywords relevant to your solution.

Across the EU, procurement data from Tenders Electronic Daily (TED) offers similar visibility.

1. ENEDIS in France and Terna in Italy are recent examples

2. They are part of multi-year digitalisation programs funded by the Recovery and Resilience Facility and the Connecting Europe Facility (CEF)

In the US, new RFPs for DER management, storage, and grid-edge communications remain concentrated at the state level, often tied to IRPs.

1. Even when they don’t convert immediately, they timestamp the next buying season.

2. FERC Order 2222 compliance filings still indicate which utilities are building distributed-energy programs.

3. Utilities publishing 2025 IRPs that include non-wires alternatives or DER orchestration are preparing to allocate funds to those areas.

For growth teams, this means we should track RFPs not only for the contracts, but for the patterns they reveal, because the pitch repeats every season. Watch who’s warming up next.

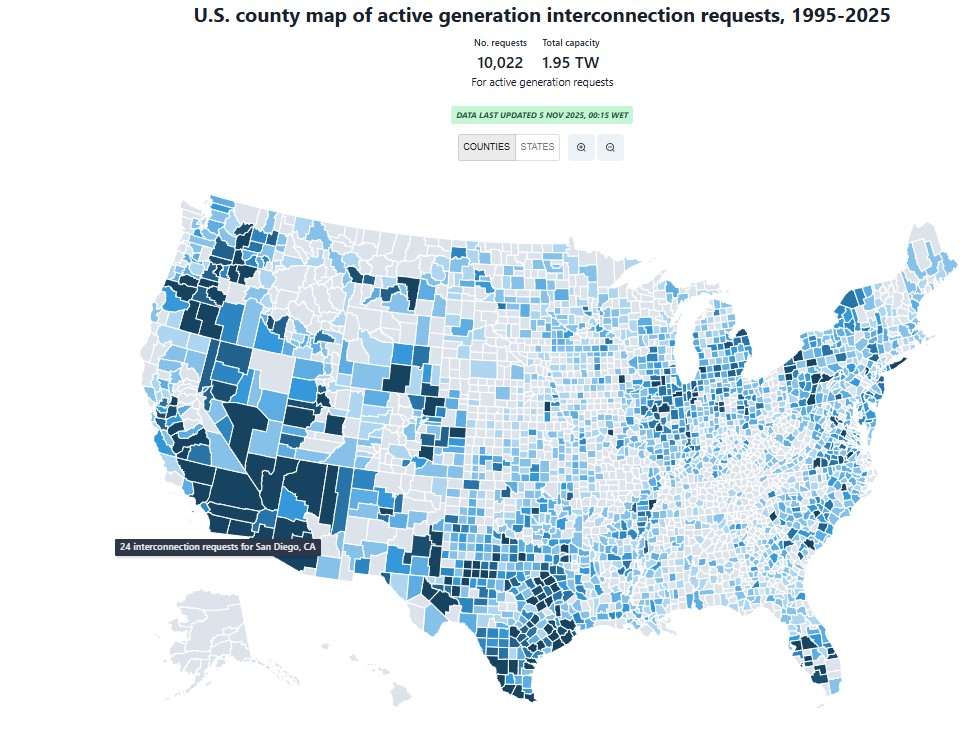

3. Interconnection and Grid-Constraint Signals

Signal strength: High, technical proof of need 🟢

When interconnection queues stack up, visibility and flexibility tools soon follow. Congestion is a leading indicator and a polite way of saying, ‘We’re about to spend money on visibility tools.”

DSOs and TSOs are publishing more data than ever: maps, queue reports, hosting-capacity dashboards, are increasingly accessible and each update is like a flare shot into the sky for those watching.

Take a look at some practical examples from around the world:

United States

1. Regional transmission organizations such as PJM and CAISO show multi-year delays and rising upgrade costs.

2. Those bottlenecks have already triggered pilots in dynamic hosting capacity, flexible interconnection, and feeder-level monitoring.

3. DOE’s DER Interconnection Roadmap (2024) calls backlogs a primary modernization driver.

United Kingdom

1. Long-Term Development Statements (LTDS) and Network Development Plans (NDPs) highlight constraint zones and trial areas for flexible connections.

2. When a DSO flags a hotspot, it’s mapping its next procurement territory.

European Union

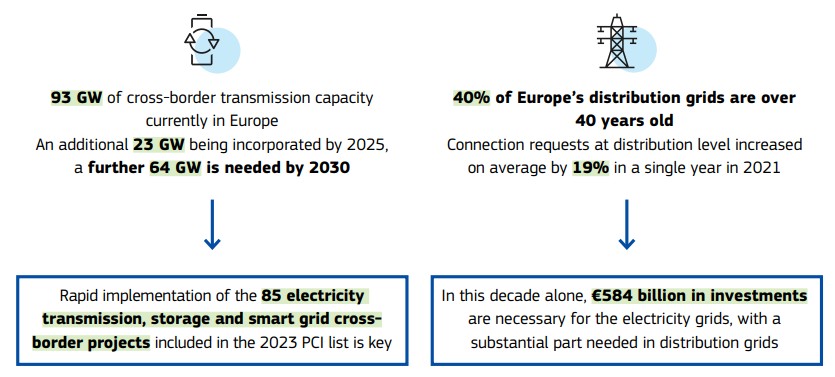

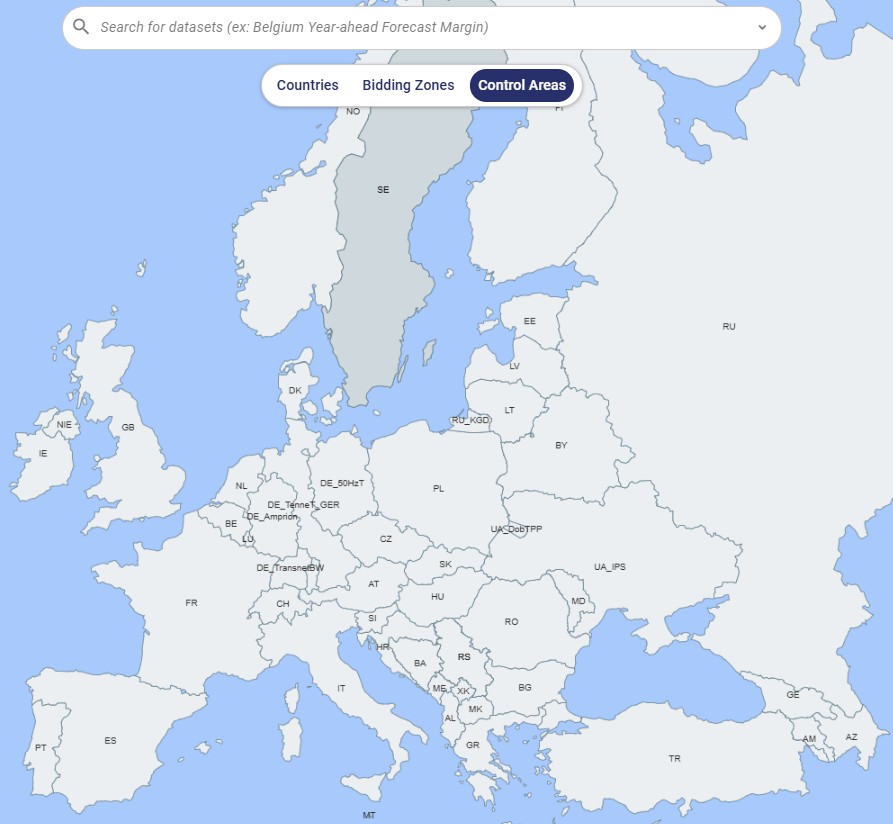

1. The new ENTSO-E transparency platform report all congestion data previously covered, but now also includes market (EUR) data,

New features include the ability to filter by market, load, generation, transmission, outages, balancing and operations.

For sales teams, seeing pressure show up in the data helps confirm that budget conversations are already underway. But if you really want to know what’s next, follow the LinkedIn and job-post breadcrumbs. Utilities love a job title before they love a pilot.

4. Talent and Hiring Signals

Signal strength: Medium: organizational preparation 🟠

Watch the hiring feed as closely as the funding feed, because the real RFPs are sometimes written in job descriptions.

Roles like DER Strategy Manager, Grid Data Architect, or Flexibility Services Lead usually appear 6 to 18 months before related tenders. They mean internal funding is already approved.

There are some regional nuances worth noting:

1. In the UK, flexibility-services and energy-data roles often precede Dynamic Purchasing System tenders.

2. In continental Europe, postings more commonly mention interoperability, data governance, or digital twins often coincide with EU-level initiatives such as Horizon Europe or the Connecting Europe Facility.

3. In the US, utilities will likely be slower to hire in new program areas since the suspension of DOE awards, but roles in distributed-energy integration teams still indicate protected budget lines.

Besides giving your sales teams clues on where to build relationships, these signals are useful because they reveal both timing and structure.

When a utility begins hiring new program managers, analysts, or data engineers, it suggests that business cases have already cleared internal review. It also provides new entry points for outreach, since these teams are typically mandated to explore external technology partnerships.

Monitoring hiring patterns is a low-cost, high-value habit. It helps identify when a utility is moving from concept to implementation and who within the organization is responsible for making that transition happen.

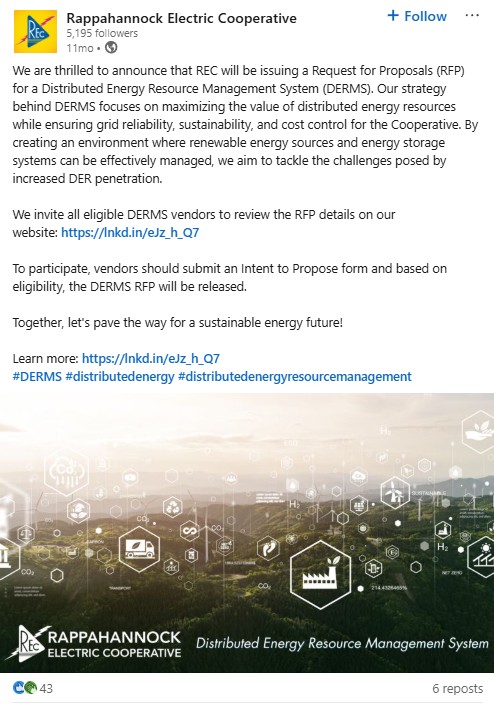

5. Partnership and Pilot Signals

Signal strength: Medium, validation before scale 🟠

Before any utility scales, it runs a small experiment. You can think of it as a safe sandbox to make sure nothing catches fire, literally or politically.

We can watch for memorandums of understanding, letters of intent, research collaborations, and participation in innovation frameworks such previously mentioned as Ofgem’s SIF, Horizon Europe, or EPRI programs. While some projects may look small, they indicate where funding and staff time are already committed.

For founders, these are early innings where each pilot proves that money, people, and permission are already in motion.

For example, DCFlex's founding members, assembled in 2024, counts some of the most important players in the utility and data center markets including Compass Datacenters, Constellation Energy, Duke Energy, the Electric Reliability Council of Texas, Google, Meta, New York Power Authority, NRG Energy, and Nvidia, among others.

Through these initiatives, DCFlex aims to develop reference architectures to promote the wider adoption of flexible practices, and will set up five to ten flexibility hubs to pilot new strategies between data centers and power providers.

How to use signals like these.

1. Log every new pilot in your target utilities.

2. Note the tech category, partners, and funding source.

3. When two or more pilots cluster around the same theme, notice the patterns as they relate to your solution.

You can use this engage early with the program teams behind them to support as needed. But of course, take every opportunity as a clue more than a done deal.

Because just when you think you’ve figured out the rhythm, the utility changes tempo.

It’s like jazz, but with regulators.

From Signal to Strategy

This is the point of inflection for gridtech, a Moneyball moment that will change the efficiency of all go-to-market teams. The teams who see early and move first will own the next season, while others struggle to keep up. To get started, you can use our framework and template to start tracking your own public and hidden signals that are revealed when your buying personas are preparing to buy, pilot, or fund new grid-modernization projects.

This template can help you:

1. Spot Demand Early: Detect procurement cycles, funding awards, and pilot programs before RFPs go public

2. Prioritize the Right Accounts: Score utilities by readiness, budget movement, and alignment with your solution type.

3. Cut Waste from ABM & Outbound: Replace guesswork with verified buying triggers that actually convert.

Get the Utility Buying Signal Tracker [TEMPLATE]

But reading the signals is only half the game.

The real edge is in systematically building these signals into your GTM strategy, so that you can act on them before the rest of the crowd even sees the pattern.

That's what we'll cover in Part III of the Gridtech Moneyball series.

Next Up: Part III — Turning signal into strategy that wins deals

Stay in the loop

Follow us on LinkedIn for more industry insights and resources to help increase your ROI.