%20(7).png)

The Valuation Discount is a number many cleantech founders rarely see until it's too late.

It's what gets applied when a Series B investor decides your GTM motion is not yet repeatable. When pipeline is built on one fragile channel, or the founder’s personal network, or on unit economics that don't work with rising Customer Acquisition Cost (CAC).

The discount represents a series of heroic acts that makes for great origin stories, but terrible board meetings. The problem is, nobody gains investor confidence after revealing that the pipeline depends on the CEO happening to sit next to the right person at a conference in Munich.

Those who cannot demonstrate go-to-market fit endure a punishing valuation, where the investor terms reflect the risk. It shows that investors are not buying a proven machine, they are buying a bet that you will figure it out with their capital, and this costs founders millions in dilution.

Today we'll look at what separates these twpo types, and how we can show up to board meetings with a strong GTM story, backed by data.

What Is Go-to-Market Fit (And How Is It Different from Product-Market Fit)?

"Series A is all about proving product-market fit and starting to craft your go-to-market strategy. At Series B you need to show GTM fit, so you can invest more heavily in the things that are already working."

— Constanza Diaz, Investor, via Carta

When Bessemer Venture Partners published their analysis of 394 cleantech companies funded during CleanTech 1.0, the headline was striking: 90% failed to return capital to investors.

The cause, they found, was commercialization. The companies that failed could not transition past the pilot phase into a working GTM system.

Successful commercialization, or the moment when a go-to-market motion becomes repeatable at scale, is the same principle Series B investors are evaluating for.

Most of the companies that died between Pilot and Development had products that worked, and markets that existed. What they lacked was a commercial system that could prove repeatability and function without the founder in every deal.

Now, the next wave of cleantech has largely learned from this, but there is a distinction still catches founders off guard.

GTM Fit means you have a repeatable, cost-efficient, scalable system for acquiring and expanding customers, and the data to prove it. Knowing which channels work, knowing what they cost to acquire customers, and knowing that it does not fall apart when we add new salespeople, spend, or markets.

%20(3).png)

When that engine is not in place, all growth becomes more risky. And for cleantech B2B, this risk can be especially brutal.

Sales cycles are long, procurement processes are non-standard. Regulatory triggers shape deal timing in ways we cannot control. Our industrial and utility procurement cycles are not the same animal as a SaaS buying motion.

So, the burden of proof on GTM fit is higher in cleantech. And providing this is possible only when we understand exactly what the board and future investors are looking at to evaluate a commercial motion.

It starts with speaking the language (read: metrics) that describe our desired end-state.

What Series B Investors Expect in a Board Meeting

Based on playbooks from Unusual Ventures, Bain Capital Ventures, and Craft Ventures, the GTM review at a Series A board meeting covers four areas:

1. Pipeline and Sales Performance

This is the most scrutinized section. The board wants to see:

1. Current quarter forecast vs. target with confidence levels

2. Pipeline coverage ratio (total weighted pipeline vs. quarterly target, with investors expecting 3-4x at this stage),

3. A deal-by-deal review of the top 5-10 opportunities

4. Conversion rates at each stage: MQL to SQL, SQL to opportunity, opportunity to closed-won.

2. Demand Generation and Marketing

Here the board wants to understand that marketing is a revenue creation function, not a brand exercise. The questions that matter are what percentage of pipeline is marketing-sourced vs. founder-sourced? What is the inbound conversion rate from demo request to qualified opportunity?

What experiments worked, what failed, and what did you learn?

3. Customer Health and Net Revenue Retention

At Series A, investors are pushing for cohort-level views of retention and expansion.

They want to see gross revenue retention (what percentage of ARR from existing cohorts survives 12 months), net revenue retention (GRR plus expansion), and logo retention, which matters especially in cleantech where customer concentration is common.

If your top five accounts are flat or at risk, that is a board-level conversation.

4. Team Capacity and Unit Economics

The board wants to know whether your sales capacity model supports the plan. How many reps are on quota? What is average attainment? What is ARR per rep, and is it improving? What is ramp time for new hires?

This determines whether the board believes you can absorb more capital productively.

"Board meetings are not sales pitches to the board. This is time to candidly discuss the good, the bad, and the ugly. If you have an experienced board, you will not scare them with anything. Intellectual honesty and transparency about the facts of reality greatly improve your chances of success."

— John Vrionis, Co-Founder, Unusual Ventures

If you cannot answer these cleanly, the board registers it and will want to follow on metrics that track progress on each front.

The Metrics That Prove Series B Readiness

Understanding what the board expects to hear is necessary, but the conversation changes when you can put specific numbers next to it.

Below are the key Series B Benchmark Metrics: NRR, CAC Payback, Burn Multiple, Pipeline Coverage, Magic Number, Forecast Accuracy, drawn from Carta Q3 2025, Benchmarkit 2025, and Rillet Q3 2025.

.png)

These numbers are drawn from B2B SaaS benchmarks, but cleantech B2B often operates with longer cycles and lumpier revenue than the median SaaS company. That means we need to contextualize them.

Qubit Capital’s research on cleantech manufacturing scale-ups notes the average Series B fundraising timeline extended to over two years in 2024. That is significantly longer than the 31-month Series A-to-B timeline HubSpot reports for SaaS.

For example, Watershed’s path to a $100M Series C was possible because they anchored their ICP to enterprises with Scope 3 reporting obligations. This was triggered by SEC climate disclosure rules and CSRD. Their demand generation strategy used those regulatory catalysts as triggers, publishing educational content upstream of compliance deadlines.

Persefoni took a different approach, focusing on procurement dynamics and sales cycle predictability, not just on who needed their product most. By targeting financial services buyers (asset managers and banks with TCFD obligations) rather than industrial buyers, they gave themselves a more uniform, faster procurement path.

The lesson is worth internalizing: the ICP that produces the best GTM metrics is not always the one with the most urgent need.

Sometimes, it is the one you can sell to most efficiently.

How to Build Revenue Intelligence for Series B

Most Series A cleantech teams I work with have the metrics somewhere.

This usually means scattered across a CRM, a marketing automation tool, a couple of ad platforms, and a spreadsheet that one person maintains.

The numbers exist, but they are not connected, they are not consistent, and they are not defensible in front of an investor.

Revenue intelligence is what we call the practice of turning that scattered data into a coherent, repeatable view of your commercial engine, built in three layers.

1. Revenue Attribution

Attribution answers the question: where did this customer come from, and what did it cost us to acquire them?

We frequently see sales cycles between 9 to 18 months and longer in our space. One specific example showed a prospect that encountered the product through a LinkedIn post, attended a webinar three months later, receiving a direct outreach from an SDR, and then finally getting re-introduced by a partner into the CRM.

The deal closed 14 months after first touch.

If the CRM records this last touch as “partner-sourced”, you lose the complete picture, and erase every upstream marketing investment from your attribution model.

%20(4).png)

This is why last-touch attribution breaks down in long B2B sales cycles, and why we need to ask better questions.

The real question is not 'how did this customer enter the CRM,' but 'how much did each channel contribute to getting them there?'

A contribution model weights each channel by the share of engagement it generated across the buyer's journey, and from there you can calculate a weighted CAC per channel that reflects what it actually costs to move buyers through the funnel.

Rather than assigning a closed deal to a single source, a contribution model weights each channel by the share of engagement it generated across the buyer's journey

From there, it becomes possible to see your true GTM picture for active and closed deals.

Divide each channel's spend by the number of closed deals where that channel had a meaningful weighted contribution. The result is a weighted CAC per channel that reflects what it actually costs to move buyers through the funnel, rather than who happened to touch them last.

---------------------------------------------------

Need help understanding your Revenue Attribution?

We run a GTM Revenue Audit that gives you a clear view of where you stand relative to industry expectations. Request yours at https://www.cleantechgrowthlab.com/contact

---------------------------------------------------

To start improving attribution hygiene today, three things matter:

- Tagging every lead at point of entry with a source and a channel

- Maintaining the source field through the entire deal lifecycle without letting sales reps overwrite it

- Running a monthly reconciliation between marketing spend and pipeline by source.

When you can show an investor your revenue contribution by channel with 12 months of clean data behind it, you are in a fundamentally different conversation than the founder who says “we think most of our pipeline comes from events and outbound.”

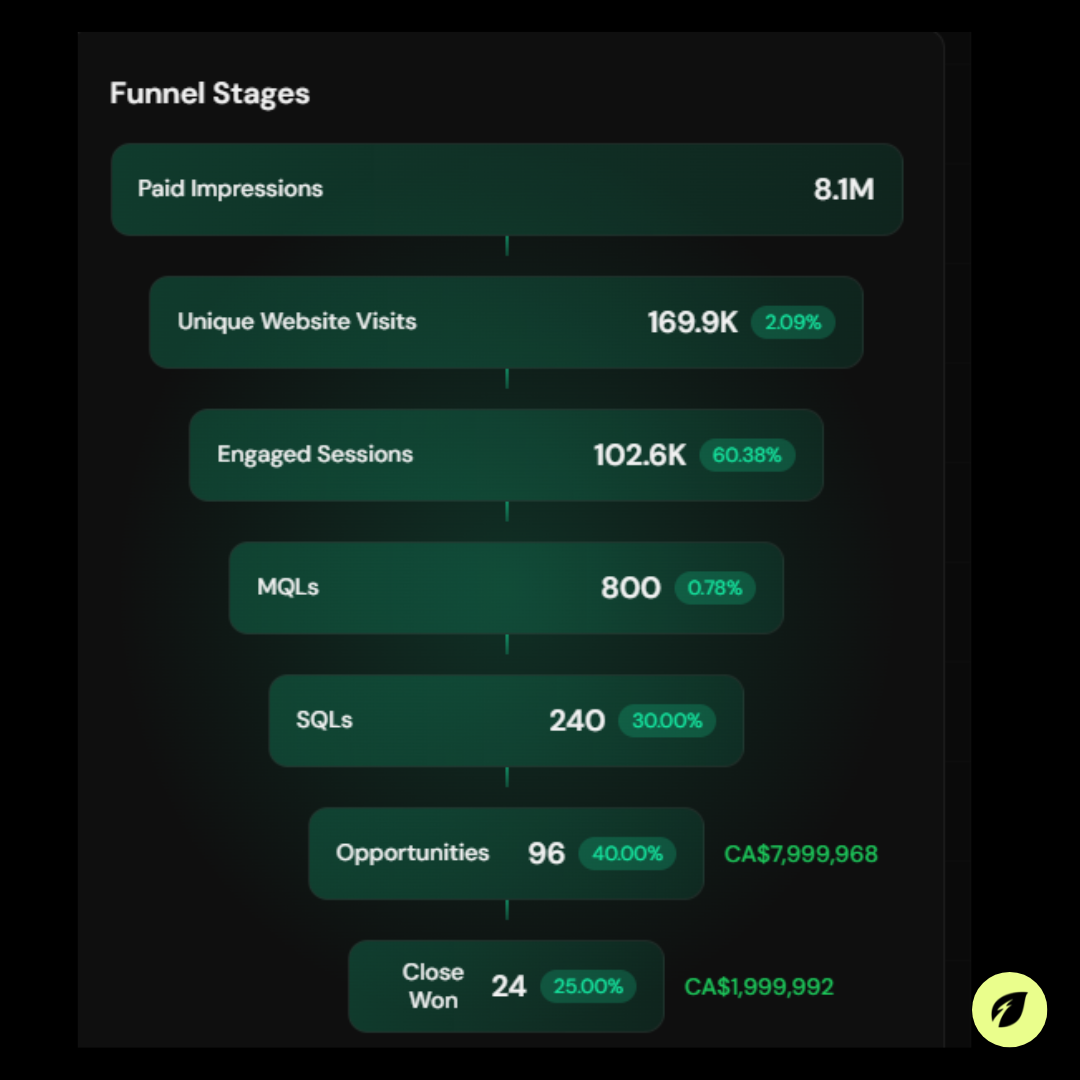

2. Funnel Stage Alignment

The second layer is making sure marketing and sales agree on what each funnel stage means and when a deal moves from one stage to the next.

One of the most common things I find in CRM audits: marketing reports 50 MQLs last month. Sales says they received 3 qualified leads.

Both are telling the truth, but marketing is counting anyone who downloaded the whitepaper. Sales is counting anyone who responded to follow-up without immediately asking to be removed from the list.

%20(2).png)

They have completely different definitions of what 'qualified' means. The board sees the disconnect and loses confidence in the data, which is worse than having no data at all.

Funnel stage alignment requires shared definitions that both teams commit to in writing. An MQL has specific criteria. An SQL has different, observable criteria. An opportunity has a defined set of conditions that must be true before it enters the pipeline.

These definitions should be simple enough that a new hire can apply them on day one, and specific enough that two people independently evaluating the same lead would reach the same conclusion.

When you present a 25% MQL-to-SQL conversion rate to the board, and it has been between 22% and 28% for the last four quarters, the investor sees repeatability. That is what GTM fit looks like in the numbers.

3. Forecast Accuracy

The third layer is the ability to predict what you will close next quarter with reasonable precision.

Each quarter, you commit a forecast. The waterfall tracks what was forecasted vs. what closed, with the delta explained. Over time, the pattern either shows improving accuracy (the team is learning to read its own pipeline) or persistent over-forecasting (the team does not understand which deals are real).

An investor can look at your NRR and CAC and see the right story. But if your forecast is off by 30% every quarter, they know the machine is not actually understood by the people running it. Consistent forecasts within 10 to 15% of actual results demonstrate that the GTM motion is not just producing revenue. It is producing predictable revenue.

The combination of these three layers, clean attribution, aligned funnel definitions, and reliable forecasts, is what makes a GTM story defensible in diligence.

Each is individually critical, but all three together is what we call revenue intelligence, and it is the difference between a board deck that reports numbers, and one that proves a system.

Series B Readiness: What to Build First

If you're reading this at month 16 and your attribution is still in spreadsheets, there is hope. But every month without clean data is a month of GTM evidence you cannot present to investors.

Of course, not every company that achieves GTM fit needs to raise Series B.

Companies that build a capital-efficient growth system can choose whether to raise, rather than needing to. Reaching profitability or near-profitability on Series A capital means that when unit economics compound instead of deteriorate, and you gain optionality.

This is only possible when the commercial engine is genuinely repeatable. The companies that treat commercial infrastructure as seriously as they treat their product are the ones that get to keep building it.

These companies share three characteristics.

- They started building the measurement infrastructure early, even when it felt premature. Revenue attribution at month 6 feels like overhead but at month 18, it is your most valuable asset.

- They contextualized metrics for their market rather than using headwinds as excuses. Long sales cycles are real, but they are no replacement for not knowing your numbers.

- They could walk an investor through the commercial engine without the founder being the only person in the room who understood it.

A founder told me last month that the hardest part of preparing for Series B wasn't building the metrics. It was admitting that the numbers he'd been presenting for 12 months were built on intuition rather than evidence.

The moment he said it out loud, the work got easier. I find that's usually how it goes.

---------------------------------------------------

Need help navigating your GTM?

We offer a limited number of free 30-minute strategic consultations. Request your consult at https://www.cleantechgrowthlab.com/contact

---------------------------------------------------

Stay in the loop

Follow us on LinkedIn for more industry insights and resources to help increase your ROI.